Recently, The New York Times Magazine ran a feature on the bail process for petty crimes, with a focus on the Brooklyn, NY court system. Although bail was historically set as a bond to ensure a defendant will return to court for trial, it is increasingly used as a tool for incarceration. According to the article, at any given time, 450,000 individuals in the U.S. are held in detention awaiting trial because they were unable to pay their court-assigned bail. A disproportionate number of these are poor.

Research from the US Financial Diaries reports many households have insufficient savings to cover bail or similar emergencies. Even a comparatively low bail of a few hundred dollars is unmanageable. In fact, 69% of USFD households below the poverty line would not have emergency savings balances high enough to post a $500 bail. Bail bondsmen, a tool used by many who cannot afford the full bail fee, often will not provide services for bail amounts of $2000 or less. So where do households turn?

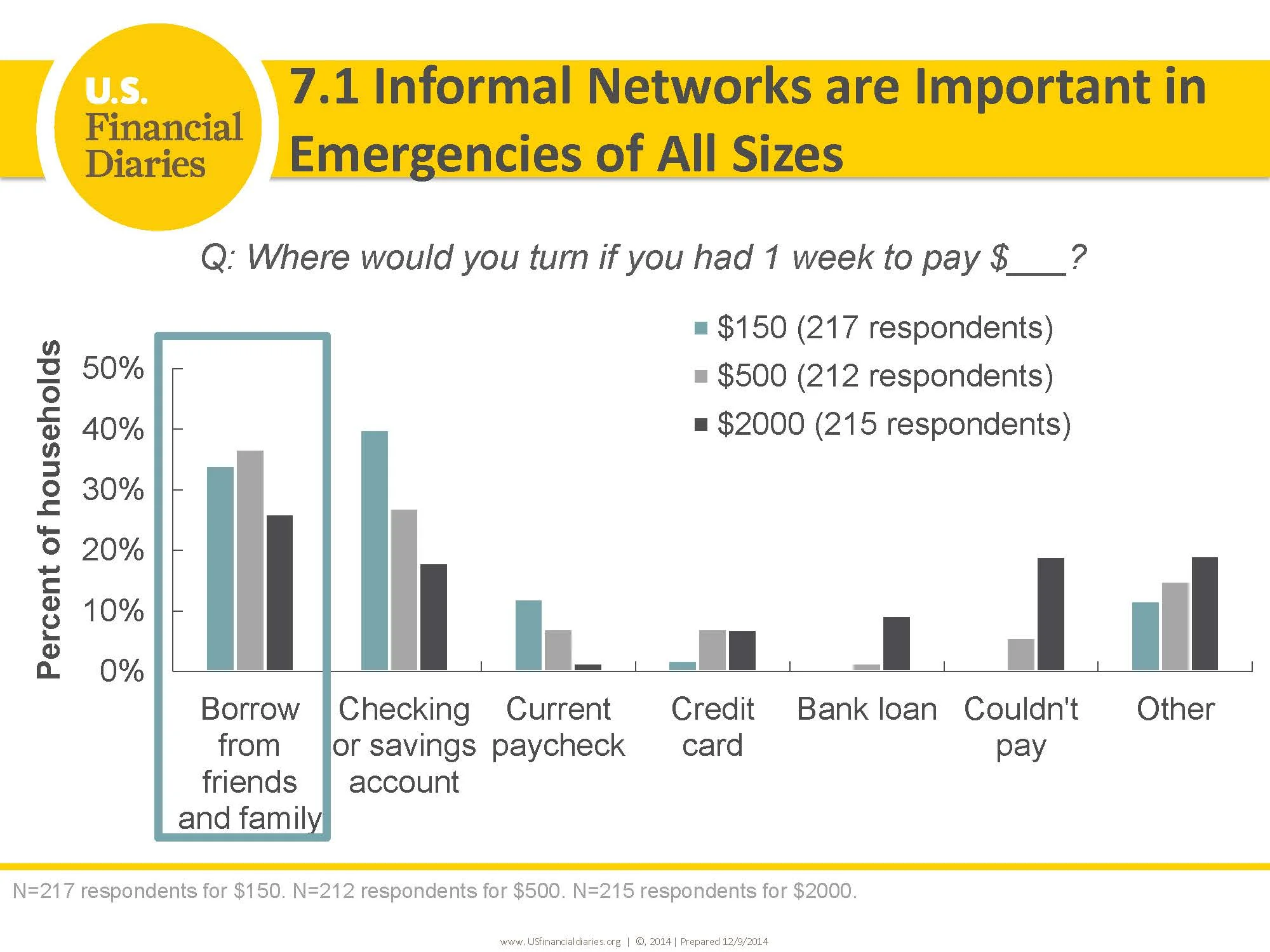

Many households rely on personal networks to cover emergency expenses, as chart 7.1 illustrates. However, as seen in chart 7.2, only 36% of households would be able to rely on friends and family as a source of emergency funds. USFD participants often cited not wanting to be in debt or feel like a burden on family or friends as a reason to avoid asking for money in a pinch.

A lack of emergency savings is not an issue that only affects low-income households. As Figure 3 indicates, 45% of all USFD families reported $0 in emergency savings. Even households that are 200% above the supplemental poverty measure struggle to save for emergencies.

Of course, emergency savings are usually measured as a balance at a specific point in time. The fact that households don’t have much in emergency savings on the day the question is asked doesn’t necessarily mean they aren’t saving. It is not simply a matter of goal-setting, financial literacy, or income that prevents households from building up and keeping savings balances.

For instance USFD households had flows into savings 4x greater than their one-time balance. A clearer picture of flows into and out of savings during the year is vital to understanding the true state of households’ ability to withstand income dips and volatile spending needs. To learn more about the savings patterns of the USFD sample, explore our Issue Briefs on emergency savings and savings horizons.

This post is part of ongoing analysis of initial findings from the US Financial Diaries. The project is lead by principal investigators Jonathan Morduch (NYU) and Rachel Schneider (CFSI). Alicia Brindisi is a research associate with the Financial Access Initiative. The views expressed therein are those of the author, and not necessarily of the USFD project or its funders.